IS RUSSIA A CROSSROADS OR AN EPICENTRE?

After a certain hiatus caused by the collapse of the Soviet Union in 1991, it is mainly through its energy policy that Russia began to actively develop its interests in the Middle East and consolidate its strategic position as a global player in the energy sector. But as events are constantly evolving, the situation can change at any time to include various scenarios for the strategic penetration of energy resources in the Middle East.

According to the latest scientific assessments, the initial estimates of gas reserves in Russia have risen to total 235.6 trillion cubic metres, of which nearly 100 trillion cubic metres stem from Western Siberia. 60 trillion cubic metres of natural gas range across the remaining areas of land and 75 trillion cubic metres are located on the continental shelf of various coastal areas and inland seas within Russia, mainly around the Arctic in the Barents and Kara Seas. For comparative purposes, consider that foreign experts affirm the world's proven natural gas reserves total only 150.2 trillion cubic meters so far, making the CIS countries’ share close to 37.8%, including Russia’s 32.1% (at 48.2 trillion cubic meters).

After Russia, Iran possesses the next largest gas reserves - about 15.3% of the world total, and Qatar comes in at about 7.4%. Turkmenistan ranks 11th overall with 1.9% of the global reserves.

Russia has taken the fact that the countries of this region are global oil suppliers into account and is actively developing its political strategy in terms of the region’s energy resources. Thus it is necessary to factor in organising the supply of oil to world markets. Most oilfields are concentrated in the Middle East and are conveniently linked to transportation infrastructure. Natural gas is another matter as the area’s sources are located almost exclusively in Russia, Turkmenistan, Azerbaijan and Iran. The competition between two projects – namely Russia’s South Stream and Nabucco, which is promoted by Western powers – is now focused on this geographical epicentre.

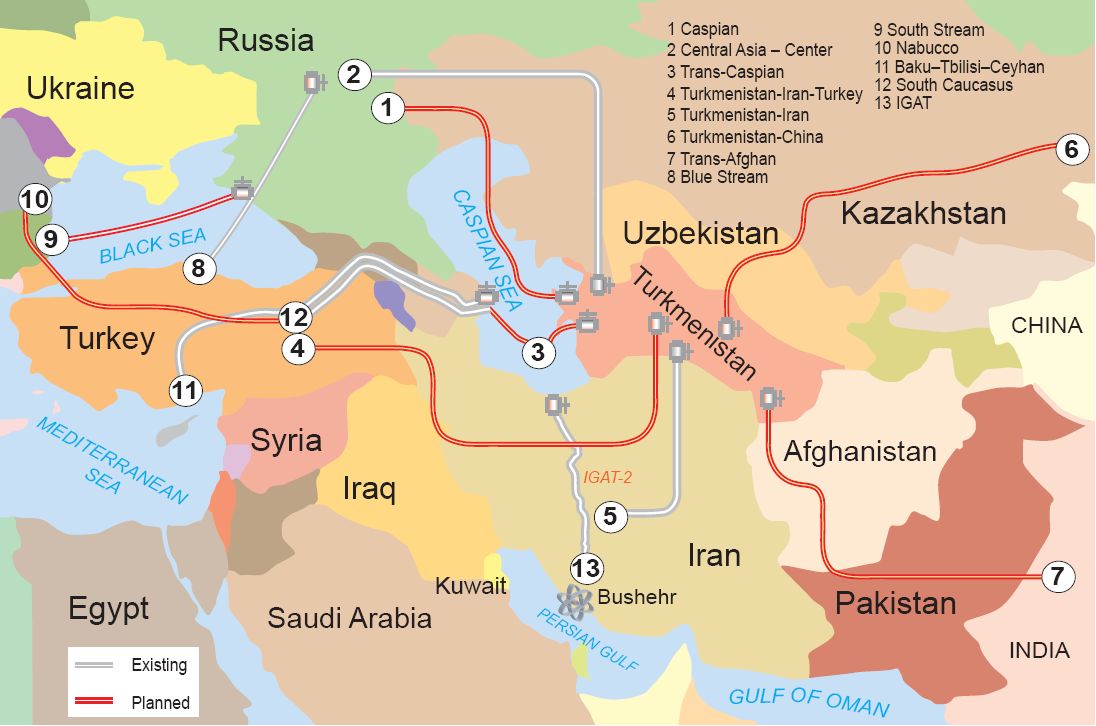

WHICH WILL COME FIRST; SOUTH STREAM OR NABUCCO?

South Stream foresees having the capacity to deliver 63 billion cubic meters of natural gas from Russian fields to the European market annually, with a potential for connecting it to Turkmen or Azerbaijani gas sources as well. Therefore, the three most important factors of this project are the availability of raw materials, connecting transit routes and the potential guaranteed demand for “blue fuel” in the EU.

Nabucco’s main route – from Turkmenistan through Azerbaijan, Georgia and Turkey to Europe – will transport just over 30 billion cubic meters of gas. Nabucco is regarded as a continuation of the existing Baku – Tbilisi – Erzurum gas pipeline. Another variant of the route is the Turkmenistan - Iran – Turkey option. However, Nabucco does not guarantee a reliable supply of gas for geopolitical reasons, mainly stemming from Iran’s nuclear program.

Turkmenistan is ready to export gas to Europe if the EU will extend its natural gas pipeline to the nation’s border.

But aside from the problems posed by Tehran, a territorial dispute over rights to resources in the Caspian Sea remains unresolved and any projects of this nature can only be discussed on a theoretical level. However, there is an alternate scenario which consists of using gas compression technology and transporting the product across the Caspian Sea in special tankers from Turkmenistan.

But it wouldn’t be sensible for Turkmenistan to ignore China’s enormous demand for energy and create a new industry given the current situation.

In the meanwhile, Russia is preparing for a new gas boom in Turkmenistan.

An agreement signed between Moscow and Ashgabat in late October calls for the two parties to adopt a policy of tactical pause and await the inevitable increase in demand for gas on the EU market. The EU Commissioner for Energy Guenther Oettinger made a statement regarding the issue, calling for the “construction of direct links with sources in the Caspian Basin over the next decade” to link the South Stream project with Nabucco.

Meanwhile, Russia has every chance of building the South Stream gas pipeline before Nabucco begins its competition.

On the other hand, Moscow is encouraging Ashgabat to participate in its Turkmenistan – Afghanistan – Pakistan – India (TAPI) gas pipeline project, which would allow the Turkmen to deliver gas to markets in Southern Asia.

Russia is willing to act as the project’s contractor, its development company and as a full member of the project’s consortium. However, it is just as important to factor in the possibility that Iran may reorient its foreign policy and that international pressure on the nation would be eased. In that case, Tehran is likely to join some Western projects in the gas sector as a potential agreement between Ankara and Tehran has already raised the possibility of both transporting Central Asian and Iranian gas via Turkish territory and using Turkish companies to develop Iran’s South Pars gas field on buyback terms.

The leading oil and gas companies are currently surveying and analysing construction projects for major gas and oil pipelines from the world's largest producers of hydrocarbons – the Middle East and Iran – to the most dynamic and developing regions of the world, which include China and the Asia Pacific countries. The concept of creating a branch pipeline to Europe is also being considered. During the initial stages, the pipeline system would pass along the Iran – Turkmenistan – Uzbekistan – South Kazakhstan – China route. In the future, the length of the route could be increased by connecting it to nations other than Iran, linking other Middle Eastern suppliers to hydrocarbon consuming countries in the Asia Pacific region. The Eurasian land transport and energy bridge may be extended in a westerly direction along the Middle East – Iran – Central Asia – Russia – Europe route, with Russia acting as a transit country.

Taking this factor into account, Russia’s Middle Eastern strategy regarding energy is based on prognostics anticipating advances in energy and economic penetration in the region, thus consolidating the Russian business community’s position there.

THE TURKISH VECTOR

This strategic penetration of energy resources and the anticipated demand for natural gas has manifested itself most noticeably in the Turkish region.

First and foremost, Turkey encompasses the important energy routes from the South Caucasus, parts of the Near and Middle East, North Africa, Central Asia, the Caspian Sea, the Balkans and the Black Sea. Secondly, Turkey neighbours the countries on whose territories three quarters of world's proven oil and gas reserves are situated. Turkey can rightfully assert itself as a West-East energy corridor or even a regional centre of power. Third, Turkey is trying to connect new pipelines to Europe from the post- Soviet states of Central Asia and particularly from Azerbaijan, which became a significant regional player with the development of the Shakh-Deniz gas pipeline - which can only transit through Turkish territory. But in terms of energy consumption, Turkey’s dependence on imports now stands at 72% and may reach 80% in 2020 although the nation has options for securing its energy supply from various sources, including from Azerbaijan via the Baku-Ceyhan pipeline.

Russia and Turkey recently reached an agreement on constructing the Samsun-Ceyhan oil pipeline and the Blue Stream-2 gas pipeline. At this point in time, Turkey depends on Russia for about 65% of its natural gas.

The important issue of diversifying resources requires the country to work on constructing a nuclear power plant, which it will be undertaking in partnership with Russia. The ‘peaceful atom’ is experiencing a boom in the Middle East; it began with the launch of Iran’s Bushehr Nuclear Power Plant, which was built with Russian assistance.

Rosatom is preparing to sign several agreements aimed at promoting international scientific cooperation in nuclear energy options with Egypt, Jordan and Kuwait soon, given the increased demand for electrical power these countries will be experiencing over the coming years.